by Charlene Crowell

(NNPA)—As Wall Street financiers attempt to defend multi-million dollar bonuses after receiving taxpayer-funded billion dollar bailouts, families throughout the country continue to struggle to keep their piece of the American dream. Every 13 seconds another foreclosure occurs. And African-Americans continue to suffer disproportionately.

|

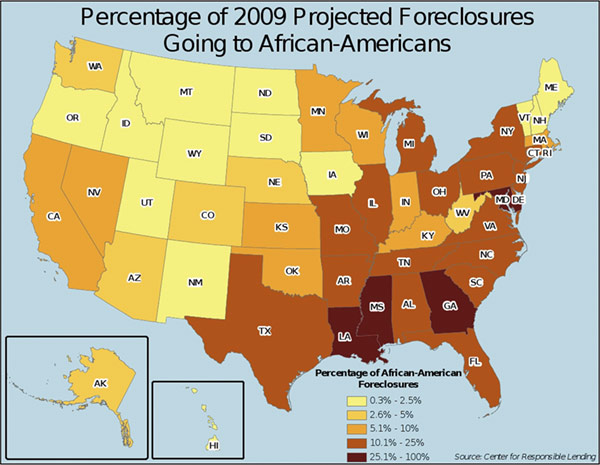

A recent analysis by the Center for Responsible Lending, an independent nonprofit research and policy organization, studied first-lien, owner-occupied mortgage loans made to African-Americans. Of the 50 states, Florida had the largest number of African-American foreclosures, with 58,474 foreclosures projected for 2009, followed by California with 32,297.

However, when CRL analyzed foreclosures as a percentage of each state’s total foreclosures, a different pattern emerged. The worst percentages for African-American foreclosures occurred in the District of Columbia, Maryland, Georgia, Mississippi and Louisiana. In 2009 alone, 301,500 African-American families will lose their homes to foreclosure. By 2012, foreclosures for Black America will affect 1,115,200 families.

Most importantly, even after CRL adjusted for the interest rate environment and borrower-related characteristics, unexplained disparities remained.

Earlier this year, CRL shared these disturbing trends with the Joint Economic Committee of the U.S. Congress. In sworn testimony, Keith Ernst, CRL director of research, told Washington lawmakers, “Empirical research shows that the leading cause of the problem was the characteristics of the market and mortgage products sold, rather than the characteristics of the borrowers who received those products.”

Continuing he added, “Even more troubling, originators particularly targeted minority communities for abuse and equity-stripping subprime loans, according to complaints and affidavits from former loan officers alleging that this pattern was not random but was intentional and racially discriminatory.”

For example, according to the Baltimore Sun, between 2005 and 2008, foreclosures involving one lender, Wells Fargo, accounted for 71 percent of foreclosed and vacant properties in mostly Black neighborhoods. The same news report also claimed that Wells Fargo made subprime loans to 65 percent of its Black customers; while only 15 percent of Whites received subprime loans.

In response, civil rights organizations, as well as state and local government officials are legally challenging lending patterns in predominantly minority communities. This past spring, the NAACP and other advocacy groups filed separate class action lawsuits in U.S. District Court against several of the nation’s largest lenders including JP Morgan Chase, Citigroup and Wells Fargo.

More recently, Illinois Attorney General Lisa Madigan filed a lawsuit alleging that Wells Fargo Bank and its subsidiaries illegally discriminated against African-American and Latino homeowners by selling these consumers high-cost subprime mortgage loans while White borrowers with similar incomes received lower cost loans.

In a statement announcing the lawsuit, Madigan said in part, “As a result of its discriminatory and illegal mortgage lending practices, Wells Fargo transformed our cities’ predominantly African-American and Latino neighborhoods into Ground Zero for subprime lending.” Madigan, along with several other attorneys general, also successfully negotiated an $8.4 billion, multi-state settlement in a predatory lending lawsuit against Countrywide, similar to a $10 million settlement this June in Massachusetts. Massachusetts Attorney General Martha Coakley successfully fought subprime lender Fremont Investment & Loan for its unfair lending practices.

Other lending lawsuits have also been filed by the city of Baltimore, and Shelby County in Tennessee. Yet, while the nation’s justice system slowly and deliberately unfolds in these and other actions, many Black Americans continue to suffer everyday from disproportionate unemployment and governmental responses that often seem too little and too late.

Ironically, as many make plans to be home for the holidays, many other American families no longer have a home to call their own.

(Charlene Crowell is the communications manager for State Policy & Outreach with the Center for Responsible Lending. She can be reached at Charlene.crowell@responsiblelending.org.)